If you’re younger than 30, chances are you’re not thinking about retirement. It’s a long way off, you’re just getting started in your career and you have your whole life ahead of you. For all these reasons, it’s the perfect time to get started on saving for retirement. You can make minimal contributions that will grow over time and allow you to retire in comfort.

While many retirees live on the money they receive from Social Security, this may not be an option for future generations. Projections show that the Social Security trust fund could be depleted by 2034. If you expect your retirement to continue after that date, you need a contingency plan. This Retirement 101 primer offers a roadmap to prepare for your future.

First, you need to figure out how much money you need to live comfortably in retirement. Here are some things to consider when planning for retirement:

Create an estimated budget for retirement that represents 80 to 100% of your current income. For example, if you bring home $5,000 a month, make a retirement budget of $4,000 to $5,000 a month. Be as detailed and realistic as possible.

Plug the numbers into a retirement calculator. This will give you a savings goal to strive toward.

Once you’ve gathered the necessary data, you can begin to explore the investment options available for retirement funds.

Matching 401(k) programs are commonly offered to workers as an employer benefit. If you haven’t started saving for retirement, start by contributing to an employer-sponsored 401(k) if available. This type of retirement fund offers several advantages:

These are some potential 401(k) downsides:

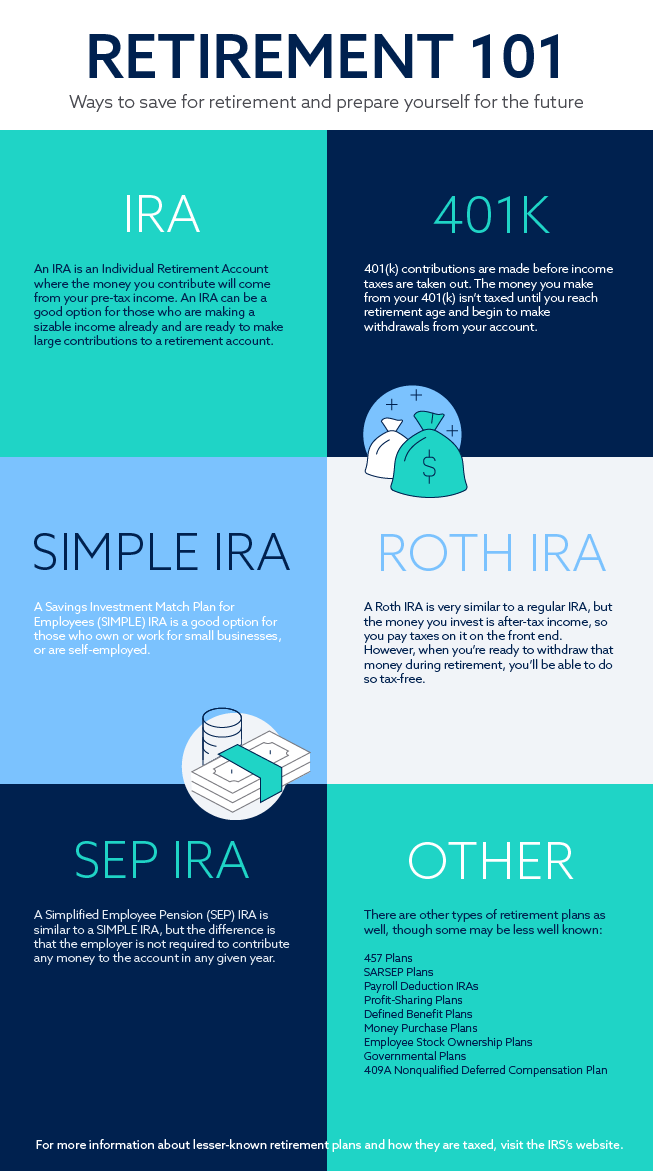

An IRA, or individual retirement account, is available to all individuals without employer involvement. Many tax experts recommend starting your retirement savings with an IRA if you don’t have an available 401(k) through your employer or if your employer doesn’t offer a matching program.

However, there are some negative aspects to an IRA:

A Roth IRA is similar to a standard IRA, but it’s funded with after-tax income. Since you’ve already paid taxes before investing in a Roth IRA, withdrawals are tax-free. For this reason, a Roth IRA is a good choice if you expect substantial income growth over the course of your career. You’ll be able to pay taxes on the investment while you’re in a lower tax bracket.

There are other advantages of a Roth IRA:

The Roth plan does have downsides as well:

Self-employed individuals and small business owners can contribute to a Savings Investment Match Plan for Employees (SIMPLE) IRA. This type of account requires a matching contribution from your employer (whether that’s yourself or a company you don’t own, but are employed by), and is taxed under similar rules as a traditional IRA. You’ll contribute pre-tax dollars, but you will be taxed when you begin to withdraw the money.

A Simplified Employee Pension (SEP) IRA is similar to a SIMPLE IRA, but does not require a matching employer contribution. Match programs that are offered must be the same percentage for each employee. Contributions made by the employer and by self-employed individuals are tax-deductible.

Although the options described above are the most common types of retirement plans, countless other plans exist. Each has unique tax advantages and disadvantages. The IRS provides detailed information about less common plans and how they are taxed.

When you get your credit score on track, you’ll save money by qualifying for lower interest rates. When less money is going toward repaying debts, you’ll have more freedom to begin building your next egg for retirement.

Take the first step on the path to a brighter financial future by repairing your credit with Lexington Law Firm. Call us today for a free personalized credit consultation to see how we can help you.

You can also start up a conversation on our social media channels. Like and follow and interact with us on Facebook, Instagram, and Twitter.

Article Updated June 2019

Learn how to get a loan with no credit. Explore secured loans, joint loans, and…

Lexington Law Firm sales representatives can no longer be contacted over the phone.

A payday loan is a short-term, high-interest loan usually due on your next payday. Learn…

With an overall 5-star rating from BestCompany, Lexington Law Firm is a legitimate company for…

The lowest credit score possible is 300. This typically happens due to negative marks on…

As of 2022, Americans aged 65 – 74 had the highest average net worth by…

{kind=link}

{kind=link}