Is Your “Clean” Credit Report Actually Hurting You?

February 11, 2026

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

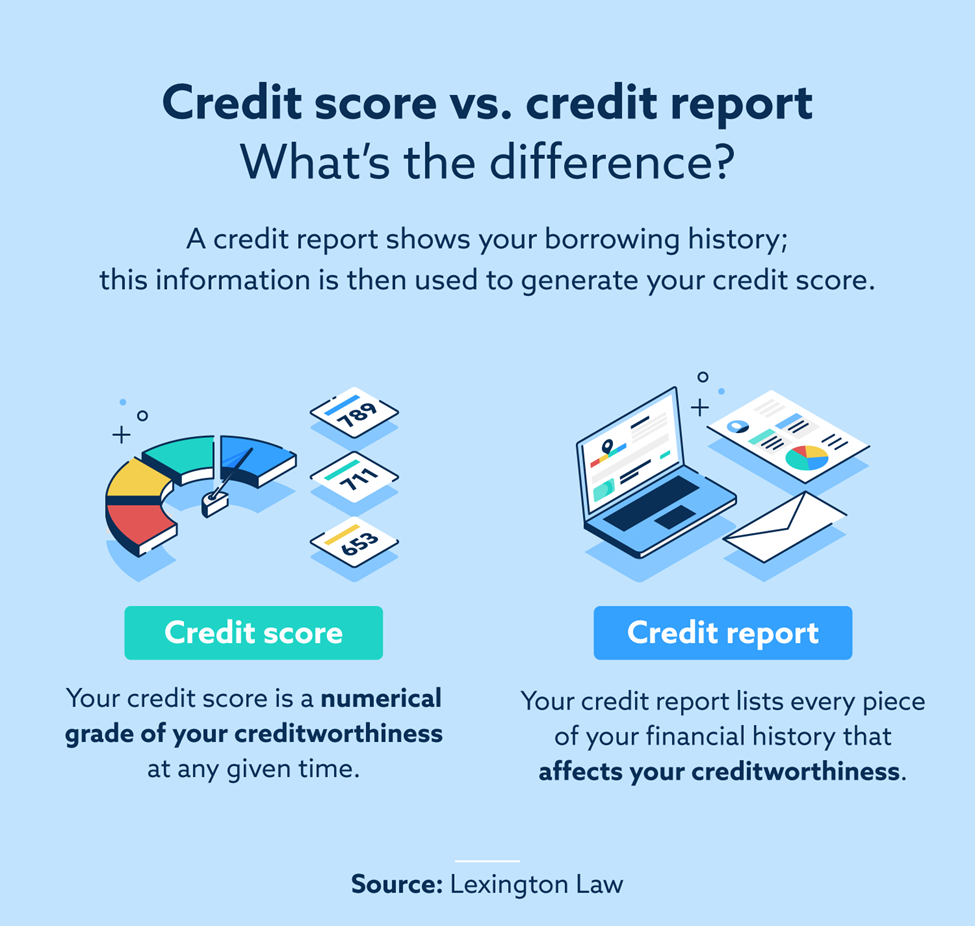

Your credit report is a detailed account of your credit history and current credit situation, while your credit score is a number calculated based on the information in your credit report. Both are used to determine your creditworthiness.

Whether you’re applying for a credit card or financing a new car, you’ve likely come across lenders asking for your credit score or viewing your credit report. These tools are both used to understand your credit risk, but there are key differences between the two. Learning how (and when) to check and manage your credit score vs. credit report is an important part of maintaining your overall financial health.

Your credit score is a number between 300 and 850 that lenders use to grade your creditworthiness, or how good a candidate you are for an extension of credit (e.g., a loan or credit card). It also determines the interest rate and loan terms you qualify for.

There are many different scoring models, but your FICO® score is most commonly used to make credit decisions. FICO® offers a variety of specialized scores for credit cards, home loans and more. Another relatively common score issuer is VantageScore®.

Credit scores are updated monthly and determined based on five main factors to predict how likely you are to be a responsible borrower, including:

This information is used to calculate your unique credit score. Keep in mind that credit scores can differ depending on the credit reporting agency, scoring model and even the day it was calculated. While scoring models vary, credit score ranges are generally quite similar. These are FICO’s scoring ranges:

Scores below 580 will severely limit a person’s creditworthiness and credit options.

Your credit report is an overview of your credit history and activity over the past seven to 10 years. This information is used to calculate your credit score, but it doesn’t include the actual three-digit number assigned to you. Credit reports include:

Three credit bureaus generate credit reports: Experian®, TransUnion® and Equifax®. You can get one copy for free from each bureau every year. It’s recommended to request these copies one at a time throughout the year to check for any potential errors that could damage your credit and hurt your chances of getting a loan.

| Credit reports | Credit scores | |

|---|---|---|

| What is it? | A detailed document listing credit activities over the last seven to 10 years | A three-digit number given to a borrower based on the information provided in their credit report |

| Who creates them? | One of the three credit bureaus (Experian, TransUnion and Equifax) | Typically FICO or VantageScore |

| How often are they updated? | Once a year | Monthly |

| What are they for? | Understanding a your creditworthiness when applying for a home or auto loan, insurance or a job | Providing a quick glance at your overall credit risk when applying for a new line of credit or rental home |

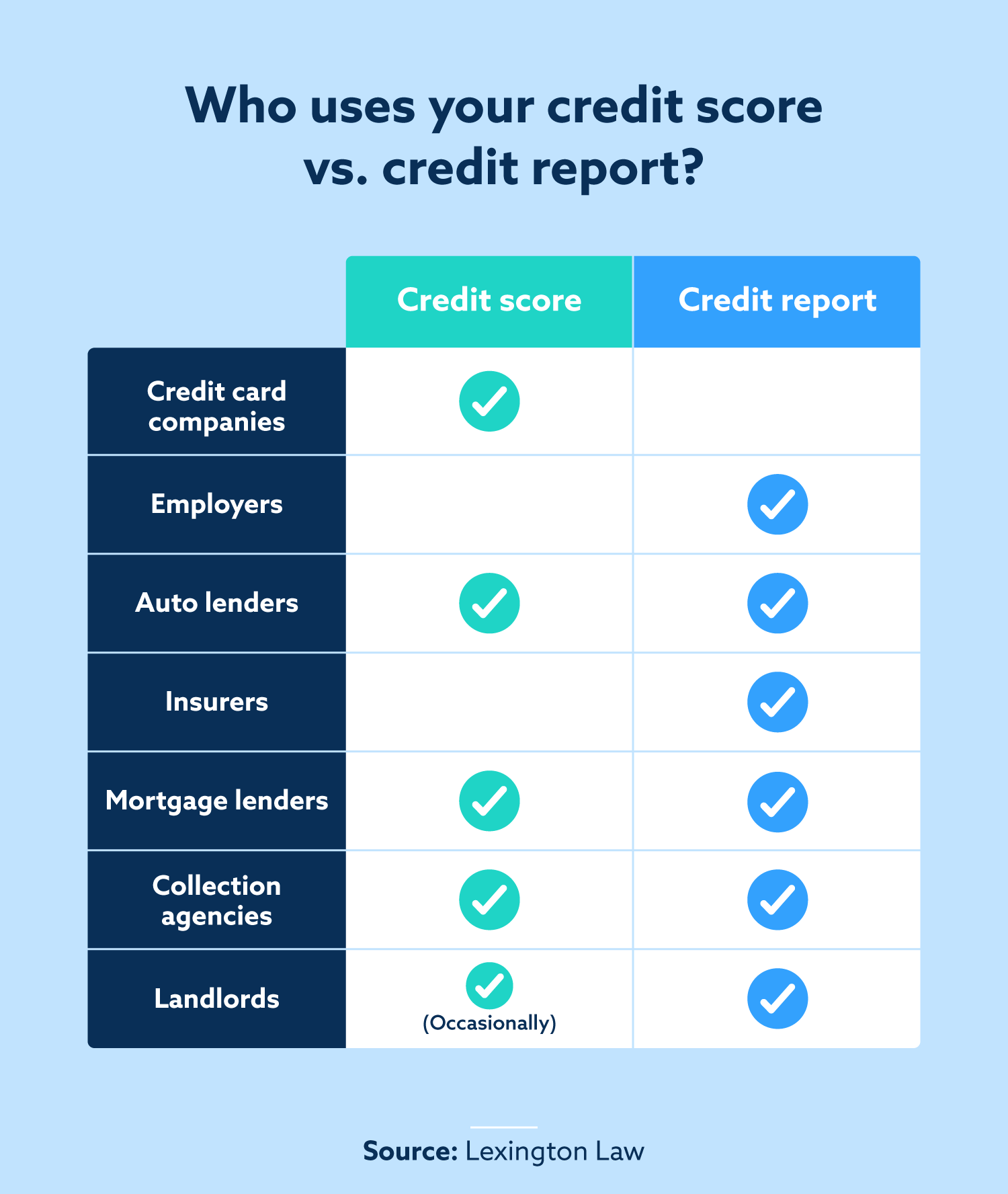

| Who looks at them? | Current and prospective creditors and lenders, prospective landlords, insurance companies, current and prospective employers, debt collectors and government agencies | Credit card companies and prospective landlords |

The main difference between a credit report and a credit score is the amount of information provided. A credit report is a detailed record of your credit history, including information about your credit accounts, payment history and public records. Credit bureaus maintain these reports, which serve as a comprehensive overview of a person’s creditworthiness.

A credit score is a three-digit number calculated based on the details in your credit report that lenders use to assess the risk of lending money to you. A higher credit score indicates lower credit risk and makes it easier to qualify for loans and obtain favorable interest rates.

When applying for a home loan, rental property or new credit card, it’s important to understand whether your credit score vs. credit report will be used to determine your eligibility. Generally, here’s who will be looking at what:

It’s recommended that you check both your credit report and credit score before applying for a new line of credit, such as a home loan, a new credit card or a student loan. This gives you a chance to see what shape your credit is in and take steps to improve it if necessary.

You can access a free credit report from each of the three national credit bureaus once every 12 months. Here’s how:

Unlike your credit report, your credit score is updated every month, and you can access it anytime through most banking sites. Contrary to popular belief, checking your credit does not decrease your score. Become familiar with your credit and look for any sudden dips that might signal possible derogatory marks.

Credit history is the foundation on which your credit is built, so it could be considered more important. A strong credit history shows responsible credit management and provides a track record of your financial behavior over time. Lenders often consider overall credit history when determining your creditworthiness, especially when evaluating applicants for larger loans or mortgages.

A “good” credit score is typically considered 670 or higher, although ranges vary depending on the credit scoring model used.

FICO and VantageScore both look at your credit history to determine your score, but they use different scoring models, resulting in slightly different grades. There are different versions of both VantageScore and FICO scores, and lenders may use different versions depending on their preferences. It’s always a good idea to monitor both scores to have a comprehensive understanding of your creditworthiness.

Knowing the difference between your credit report vs. credit score is just one of the many credit fundamentals that will help you when it comes time to make important financial decisions. From buying your first home to investing in your child’s college education, understanding and continuously improving your credit history is essential to securing your financial future.

Lexington Law Firm can help you evaluate and understand your credit report, so you know what steps you need to take to improve your credit and reach your financial goals. Our team offers credit repair and credit education services so you don’t have to navigate these challenging situations on your own.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.