The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

There are at least 16 distinct versions of FICO scores currently in use, with new ones potentially developed to cater to the specific needs of different industries and consumers.

FICO scores are a crucial element in understanding your credit health and working towards improvement. They consider several factors on your credit report, like payment history, credit utilization ratio and length of credit history. They play a major role in determining your loan approval odds and interest rates.

However, unlike a single credit report, there isn’t just one universal FICO score. FICO offers a range of scores, typically falling between 300 and 850, tailored to specific credit card types, loan applications and industries. Understanding the different types of FICO scores and what they represent empowers you to manage your credit effectively and achieve your financial goals. Below, we’ll explore the different types of FICO scores and what they mean for you.

Table of contents:

- How many types of FICO scores are there?

- Why are there various FICO score versions?

- How are FICO scores calculated?

- How to check your FICO score

- Which FICO score should you check?

- How to improve your FICO score

How many types of FICO scores are there?

FICO offers a range of scores, with reports of at least 16 distinct versions currently in use. These variations cater to specific credit needs like mortgages, auto loans or credit cards. It’s important to note that even though there are multiple FICO scores, credit scores generally play a major role in determining your loan approval odds and interest rates.

While you have one credit history, the story behind your credit score can vary slightly depending on the credit bureau. This is because Experian®, TransUnion®

and Equifax® might not receive the same information from all creditors. As a result, each bureau might generate a slightly different FICO score for you.

FICO scores 8 and 9

FICO Scores 8 and 9, developed in 2009 and 2017, are the two most widely used versions. These scores provide a more sophisticated analysis of your creditworthiness compared to earlier models. While both consider factors like payment history, credit utilization and credit history length, FICO Score 9 gives recent credit activity slightly more weight.

They’re the go-to choice for lenders across various loan types, including mortgages, auto loans and personal loans. A strong showing in either FICO Score 8 or 9 significantly boosts your chances of loan approval and potentially unlocks more favorable interest rates.

FICO score categories by industry

Beyond the base FICO scores, there are also industry-specific versions tailored to assess creditworthiness within a particular sector. Industry-specific examples include:

- FICO scores for auto lending: FICO auto scores place greater emphasis on your history of making car payments on time and managing loan balances. They’re less concerned with your overall credit card utilization compared to your base FICO score.

- FICO scores for mortgage lending: FICO mortgage scores delve deeper into your long-term financial stability. Factors like your employment history and housing stability carry more weight than a base FICO score.

- FICO scores for credit card lending: FICO bankcard scores focus heavily on your revolving credit history. They weigh your credit card balances and payment behavior on existing cards more heavily than a base FICO score.

Keep in mind: New FICO score versions are released periodically, so you might encounter industry-specific scores tailored to other lending sectors.

| Experian | Equifax | TransUnion | |

|---|---|---|---|

| Scores most widely used | FICO® Score 9, FICO® Score 8 | FICO® Score 9, FICO® Score 8 | FICO® Score 9, FICO® Score 8 |

| Scores used for auto lending | FICO® Auto Score 9, FICO® Auto Score 8, FICO® Auto Score 2 | FICO® Auto Score 9, FICO® Auto Score 8, FICO® Auto Score 5 | FICO® Auto Score 9, FICO® Auto Score 8, FICO® Auto Score 4 |

| Scores used for mortgage lending | FICO® Score 2 | FICO® Score 5 | FICO® Score 4 |

| Scores used for credit card lending | FICO® Bankcard Score 9, FICO® Bankcard Score 8, FICO® Bankcard Score 2, FICO® Score 9, FICO® Score 3 | FICO® Bankcard Score 9, FICO® Bankcard Score 8, FICO® Bankcard Score 5, FICO® Score 9 | FICO® Bankcard Score 9, FICO® Bankcard Score 8, FICO® Bankcard Score 4, FICO® Score 9 |

| Newly released scores | FICO® Score 10, FICO® Auto Score 10, FICO® Bankcard Score 10 FICO® Score 10T | FICO® Score 10, FICO® Auto Score 10, FICO® Bankcard Score 10 FICO® Score 10T | FICO® Score 10, FICO® Auto Score 10, FICO® Bankcard Score 10 FICO® Score 10T |

Why are there various FICO score versions?

While a single FICO score might seem ideal, the reality is that different credit needs require a more nuanced approach. Here’s why we have various FICO score versions:

Evolving technology

The way we use credit is constantly evolving. This evolution happens through periodic updates that incorporate new analytical tools for improved risk prediction. These updates result in new FICO score versions being released. Lenders can choose whether they’ll adopt the latest version or stick with their current one.

Industry specificity

Not all loans are created equal, and neither are FICO scores. For example, a FICO auto score prioritizes your car payment history, while a FICO mortgage score focuses on long-term stability, like employment history. These industry-specific scores give lenders a more clear picture of your ability to repay the specific loan you’re applying for.

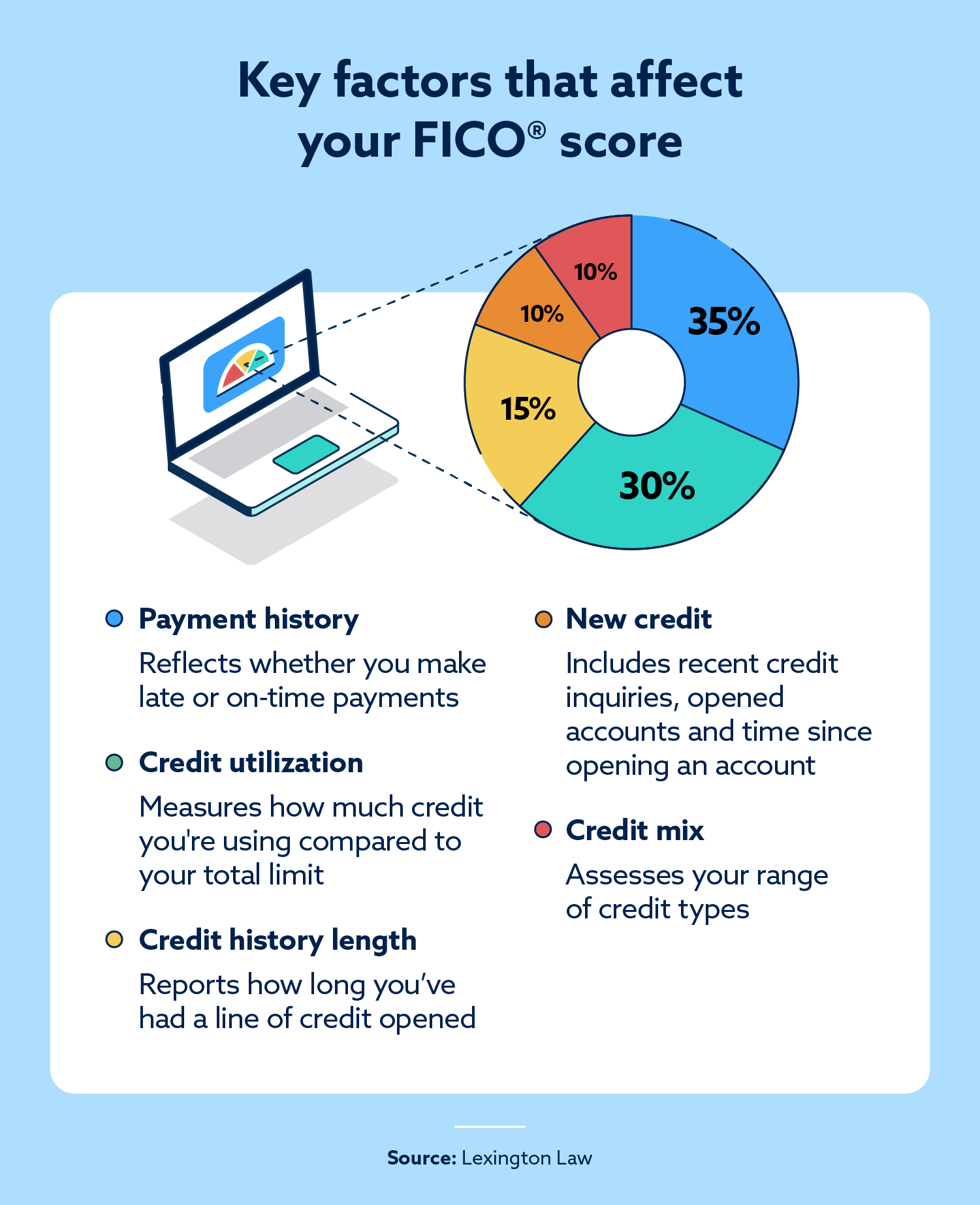

How are FICO scores calculated?

These scores are derived from information in your credit reports maintained by the three major bureaus: Experian, TransUnion and Equifax. While specific weightings vary between FICO versions, all scores rely on five key factors from your credit history. Below is a breakdown of the factors considered in one popular model, FICO Score 9 and their approximate weightings:

- Payment history (35 percent): This is the most crucial factor. It reflects your track record of making timely payments for credit cards, loans and other obligations. Late payments or delinquencies can significantly lower your score.

- Credit utilization (30 percent): This refers to the amount of credit you’re using compared to your total credit limit. You should ideally keep your utilization below 30 percent.

- Credit history length (15 percent): A longer credit history with responsible management generally translates to a higher score.

- New credit (10 percent): Applying for multiple lines of credit in a short period can temporarily lower your score.

- Credit mix (10 percent): Having a healthy mix of credit types, such as credit cards and installment loans, can positively impact your score.

By monitoring your credit reports and focusing on these key areas, you can work toward a strong credit score, make informed decisions to improve your FICO score and achieve your financial goals.

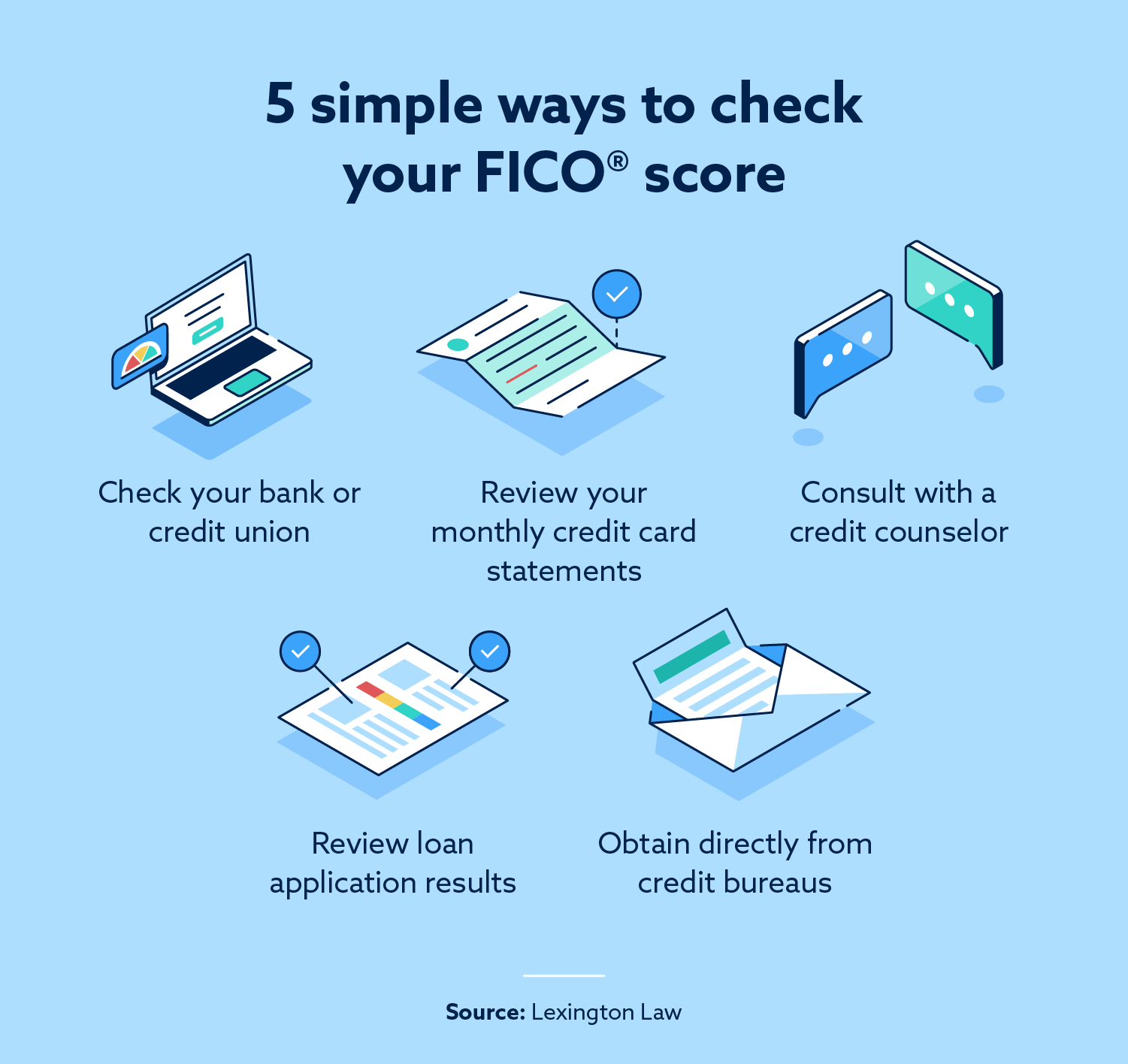

How to check your FICO score

Knowing your FICO score is crucial for taking charge of your financial health. Here are some ways to access your score:

- Check your bank or credit union: Look online or within your mobile banking app to see if this option is available.

- Review your monthly credit card statements: Some credit card issuers include your FICO score or a variation, such as Vantage Score, on your monthly statements. Review the details to understand any associated fees.

- Consult with a credit counselor: Non-profit credit counseling agencies can provide guidance on your credit report and may offer access to your FICO score as part of their services.

- Review loan application results: When applying for certain loans, lenders may provide your FICO score as part of the application process.

- Obtain your score directly from credit bureaus: You can access a free credit report from each of the three major bureaus (Experian, TransUnion and Equifax) annually at Annual Credit Report.

Important note: While some services might advertise a “free” FICO score, be cautious of any hidden fees or recurring charges associated with signing up for additional features. It’s always best to read the fine print before entering any personal information.

Which FICO score should you check?

Since your credit report information from all three major bureaus (Experian, TransUnion and Equifax) influences your FICO scores, you’ll want to check your credit report from each bureau. Lenders have the flexibility to utilize any version they deem appropriate for the specific loan type. This can make it challenging to pinpoint the exact score a particular lender might use.

Many bureaus offer a glimpse of the FICO scores associated with your credit report, giving you a general idea of the range you might fall within. While you might not know the exact version a lender will use, focusing on improving your overall credit health across all factors will positively impact all your FICO scores, ultimately strengthening your scores.

How to improve your FICO score

How do you reach for a fair credit score (typically 640 to 699) or climb even higher? Here are key strategies you can implement:

- Make payments on time: Delinquencies and late payments significantly lower your score. Focus on making all your credit card bills and loan payments on time, every time. Set up automatic payments to avoid missed due dates.

- Don’t close old accounts abruptly: A longer credit history generally translates to a higher score. Don’t make the mistake of closing old credit card accounts once they’re paid off. The length of your credit history, with a positive track record, is valuable.

- Dispute errors on your credit report: Review your credit reports regularly and dispute any errors you find. Inaccurate information can negatively impact your score. The three major bureaus (Experian, TransUnion and Equifax) each have an online dispute process.

- Keep balances low: Don’t max out your credit cards. Strive to keep your credit utilization ratio low, ideally below 30 percent of your credit limit. This demonstrates your ability to manage credit responsibly.

While results may vary depending on your credit history, consistently following these steps can help raise your score.

Understanding your FICO score is important to ensure you’re on track for a healthy financial future. Sign up for your free credit assessment and see where you stand in your credit journey.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.