The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Debt collection scams are common and come in many forms. In 2023, the FBI reported that $394 million dollars were stolen by criminals pretending to be government agencies.

The best way to protect your hard-earned funds from scammers is to learn the telltale signs.

In this guide, we’ll explore several common scams and share strategies for protecting your funds. We’ll also discuss Lexington Law Firm’s credit snapshot tool, which can help you learn which debts you genuinely owe.

Key Takeaways:

- Congress created The Fair Debt Collection Practices Act (FDCPA) in 1977 to prevent aggressive debt-collection practices.

- A collections agency is likely legitimate if it can provide its name, number and mailing address.

- You can stop debt collection scams by declining to share sensitive information over the phone, via email, and by confirming the debt actually belongs to you.

What does a debt collection scam look like?

Debt collection scams can be very subtle. You might abruptly receive a text or a phone call from someone who claims to represent a collections agency or even a government institution. The collector might rapidly hurl information at you with the intent to disorient and deceive.

Scams can also look like someone “confirming” sensitive information like your banking account details and Social Security number. It’s best to exercise caution and patience here; try not to let a caller pressure you into acting or giving out personal information before you’ve verified their identity.

Bottom line: Don’t share your personal or financial information when you receive a call, as scammers can use these details to steal your identity or convince you to send them money.

How do I know if a collection notice is real?

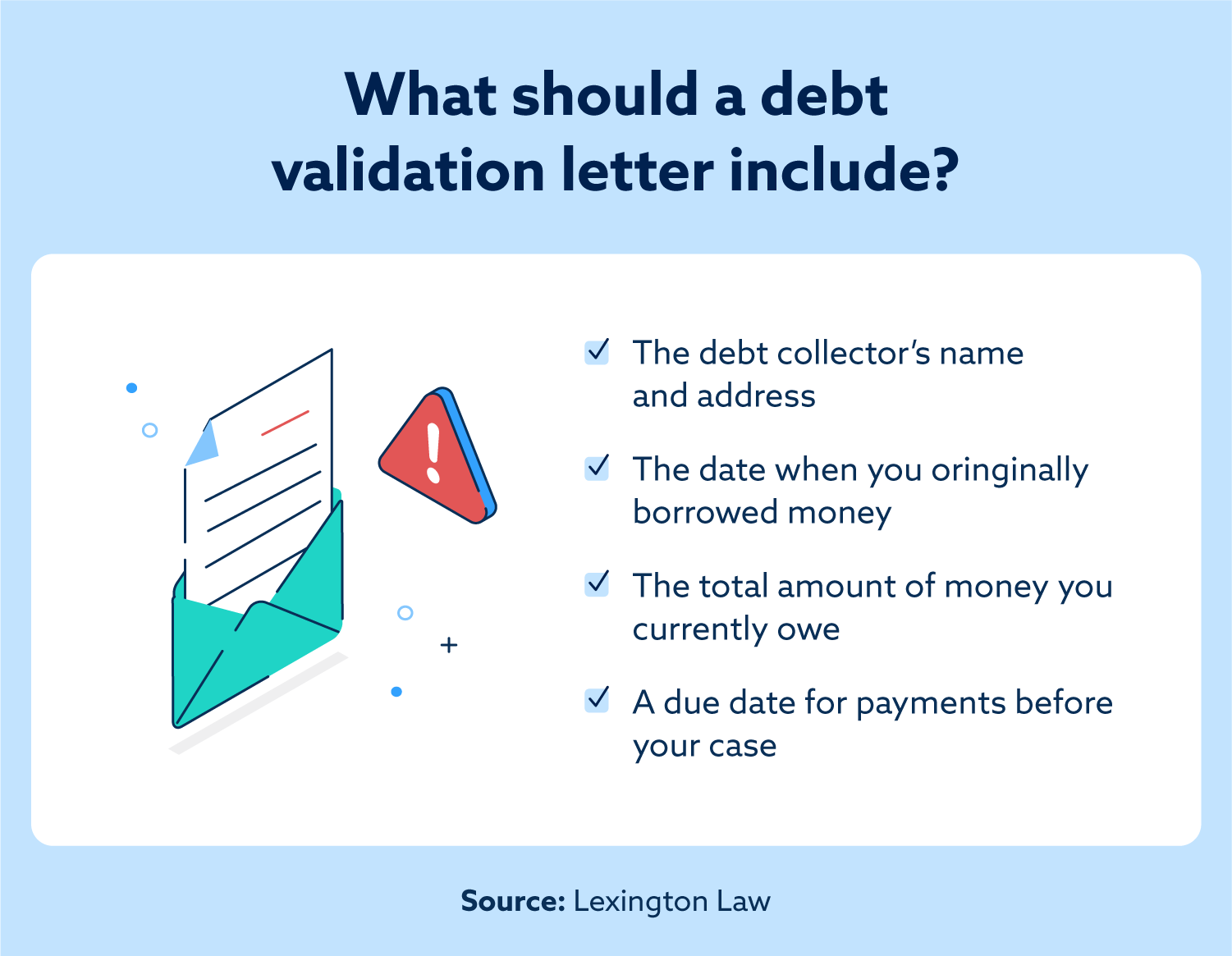

When you’re first contacted about a debt, make sure that you ask the caller to verify the debt by sending a written debt validation letter. By law, debt collectors must send you information about how much you owe and who the original creditor for the debt was.

Once you’ve received the letter, you can verify that the debt legitimately belongs to you, following up with the original creditor if necessary. If the debt collector refuses to provide debt validation, it’s likely that they are not authorized to collect the debt — or the debt never existed in the first place.

Bottom line: The law requires debt collectors to provide a validation letter for any legitimate debt.

3 tips to stop debt collection scams

Debt collection scams can take on many forms, but vigilance plays a big role in reducing their impact. If you suspect that a scam is at play, consider the following advice.

1. Get additional details from the collector

When thinking about how to deal with debt collectors, asking for additional details can help you determine an agent’s legitimacy. Remember to ask the collector you’re speaking with for the following information:

- The collector’s name

- The agency they claim to work for

- Said agency’s website

- The address where they’re located

- The collector’s email address and their agency’s email

Some callers also identify themselves as members of law enforcement or attorneys. In those cases, ask for names, badge numbers, agencies or law firms. If a caller indicates that a lawsuit has been filed against you, ask for the court where the suit was filed as well as the case number.

In most cases, scammers will be unwilling or unable to provide all of this information. If you do get specific information, you can follow up by calling creditors or law enforcement directly to verify the claims.

Knowing the status of your collections account is another powerful strategy, especially if your bank or lender has never told you that your debt has gone to collections to begin with. Check your credit report or contact your bank to see if you owe any money to collections agencies.

Bottom line: Press the collector for specific details, like their name and the collection agency they work for.

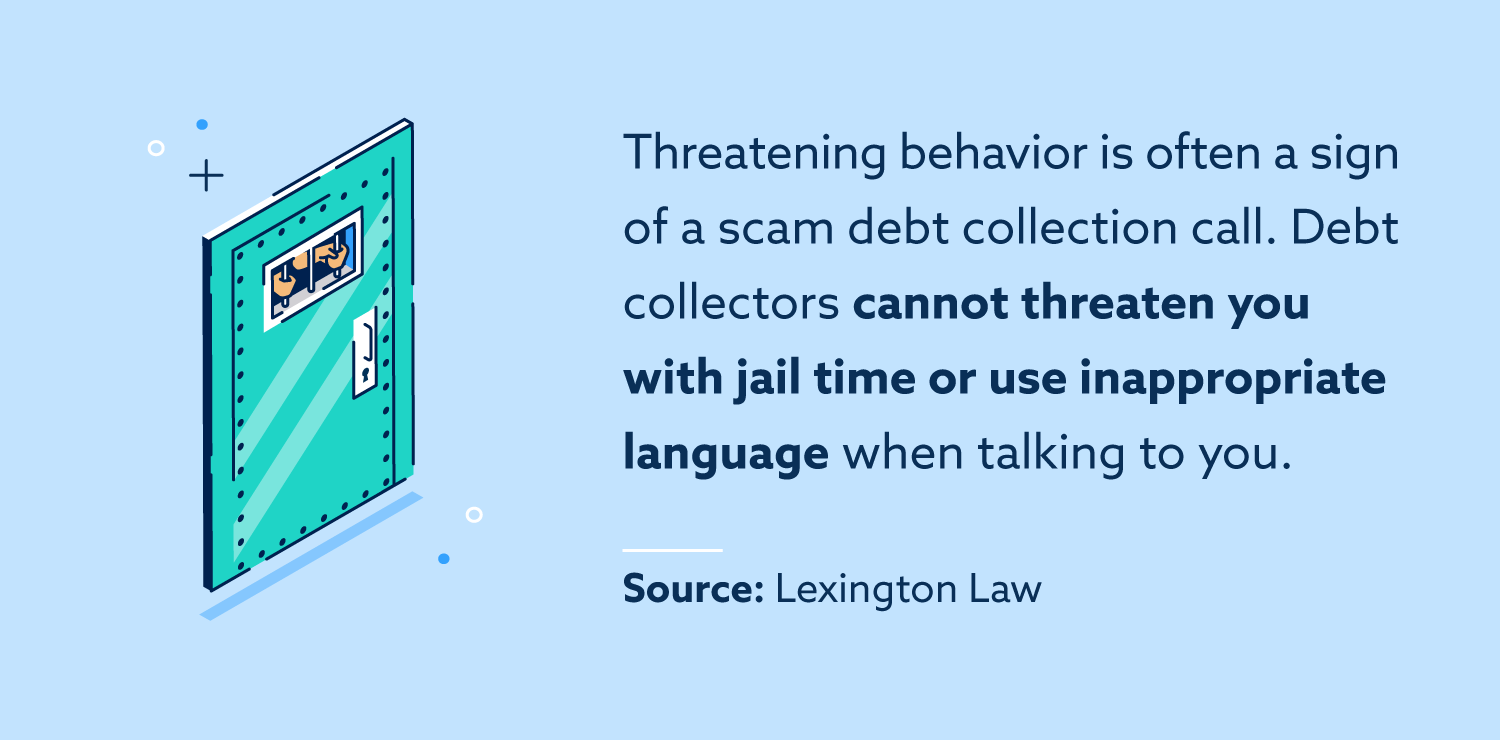

2. Watch out for threatening behavior

Sometimes, scam debt collectors will pressure you to pay quickly over the phone. Often, they’ll use serious claims to motivate you to act quickly — for instance, they’ll tell you that you have a warrant for your arrest, or you will serve jail time if you don’t pay immediately.

Scammers may also tell you that others in your family may suffer consequences, that you will lose your job or that your debt amount will skyrocket if you don’t provide payment over the phone. Debt collectors cannot send you to jail or make threats for non-payment.

Whether the debt collector is legitimate or not, threatening behavior is never permitted. Federal law specifically governs how debt collectors must behave, so you have recourse regardless of whether the debt is legitimate. If you believe the debt collector is a scammer, simply stop engaging until you receive debt validation. On the other hand, if the debt collector is legitimate but behaving in a threatening way, you can file a complaint with the Federal Trade Commission (FTC).

Bottom line: Debt collectors are forbidden by law to threaten you, and extreme claims about jail time or immediate need for payment are often indications of a scammer.

3. Block or ignore repeated calls

If you’re receiving numerous debt collection scam calls, consider blocking or ignoring these calls. Here are a few tips for blocking spam calls:

- Watch out for “spoofed” numbers. The number a scammer calls from rarely belongs to them — instead, they temporarily use someone else’s number. Be wary of unfamiliar numbers that start with the same six digits as your own.

- Some carriers and phones offer spam-blocking software. Call your cellphone carrier and ask if they have any features for blocking spam calls or search your phone’s app store for highly rated apps that can block spam calls.

- Only accept calls from known numbers. Many phones allow you to only accept calls from trusted contacts, sending all other callers to voicemail. This feature can be helpful, as many scammers won’t leave voicemails or will leave robotic voicemails that can simply be discarded.

If you do need to accept calls from unfamiliar numbers — for instance, because you’re waiting for an important phone call — make sure that you’re careful when answering the phone.

If a caller identifies themselves as a debt collector, keep it short. If you don’t have any outstanding debts, simply say, “This debt does not belong to me,” and hang up. If you know that you have legitimate debt, ask for a validation letter and contact information, then end the call.

Bottom line: If possible, ignore calls from unfamiliar numbers or install spam call-blocking software on your phone. If you do accept a call from someone claiming to be a debt collector, keep the conversation short.

Know your debt collection rights

The Fair Debt Collection Practices Act (FDCPA) is a federal law that outlines exactly what debt collectors can and cannot do. Understanding debt collection laws offers two benefits: First, you can identify callers who violate these practices as possible scammers. Second, you can file a complaint against a legitimate collector who violates the law.

Watch out for any of the following behaviors, which are prohibited by federal law and could indicate a scam debt collection call:

- Calls outside of the hours of 8 a.m. and 9 p.m.

- Uses profane or inappropriate language

- Makes false claims about your debt

- Refuses to identify themselves or their company

- Claims that you will pay penalties or face punishment for not paying immediately

- Fails to provide debt validation

Most legitimate collection agencies follow the FDCPA guidelines when contacting people, so be wary when talking to anyone who is aggressive or unwilling to provide additional details.

Bottom line: If you’re dealing with a scammer, they likely won’t honor federal laws about debt collection — so make sure you know your rights and avoid scams.

Keep an eye on your credit reports

For your best chance of avoiding scammers, make it a habit to check your credit reports at least once a year and more often if you’re actively rebuilding your credit.

By reviewing your reports regularly, you’ll know whether you have any outstanding debts — so if a debt collector calls, you’ll be ready to ask for validation. Additionally, checking your credit reports frequently enables you to spot any fraudulent or inaccurate accounts listed on your reports.

Once you’re armed with knowledge about your credit, collection laws and common tactics used in scams, you’ll be prepared to stop debt collection calls with ease. Just remember to:

- Ask for debt validation and contact information

- Avoid providing personal information on the phone

- Watch out for red flags like threatening behavior

Bottom line: Staying on top of your credit reports will help you avoid scams and know when you have legitimate debts to pay.

What to do if you’re the victim of a debt collection scam?

Today’s scammers can be quite convincing, so many people fall victim to fake debt collection calls by providing personal information, financial information or even payment.

If you’ve been the victim of a scam, act quickly by taking the following steps:

- Freeze your credit: Contact the three credit bureaus and ask them to freeze your credit immediately — that way, no one can open a new line of credit in your name.

- Watch out for identity theft: File a report with the Federal Trade Commission and IdentityTheft.gov.

- Contact your bank and credit card providers: Get new credit cards and change your bank account information if it has been compromised.

You should also change account passwords for your email and financial accounts. Finally, consider contacting local law enforcement to report the scam.

Having your identity stolen can lead to fraudulently opened accounts, so you’ll want to ensure that your credit reports do not contain any misleading information. The work of a scammer could damage your reputation, so make sure you stay vigilant about monitoring your credit if your information is stolen.

Often, it can be helpful to work with a credit repair company to review your reports and file disputes after a scam. Consider reaching out to the credit repair consultants at Lexington Law Firm, who specialize in credit repair and communicate with the bureaus to ensure your information is accurately reported.

Manage your debt with Lexington Law Firm

It’s much harder for scammers to take advantage of you if you know what you owe. Lexington Law Firm offers many different services for credit monitoring and debt repair. If you unfortunately experience identity theft, our focus tracks can help you develop a recovery plan.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.