The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

A good business credit score can strengthen a company’s financial position and make it easier to qualify for loans to grow and expand. For new businesses, lenders typically base their decisions on the business owner’s personal credit score, so getting those loans may be difficult.

Building business credit with bad personal credit is possible and can help strengthen loan applications and increase business owners’ chances of qualifying for the financing they need to grow their brands. Let’s look at how business owners can improve their business credit scores even when their personal credit scores aren’t perfect.

Key takeaways:

- Creating a clear separation between personal and business finances can aid in your credit-building efforts.

- Vendor credit, secured business credit cards and alternative financing options provide starting points to establish a positive credit history.

- Timely payments, responsible credit use and credit monitoring will steadily improve your credit profile.

How bad personal credit impacts business credit

Business credit is similar to personal credit as it gives lenders and credit card issuers insight into your financial strength and habits. Like personal credit scores, a business’s credit score can go up with good financial behaviors like paying down loans and making credit card payments on time.

This differs from personal credit because it reflects the business’s credit history, not the business owner’s or owners’ credit histories. However, business credit is something that’s built over time. When a company is just starting out, it’s not uncommon for lenders to use personal credit scores to evaluate the business’s creditworthiness.

Lenders will view a business more favorably if it has a good personal credit score. After all, a business owner who is capable of paying off personal debts and credit cards is likely to do the same for their business.

For business owners with bad credit scores, getting financing to start their business can be difficult. Lenders may charge higher interest rates on loans or offer smaller loans to reduce their risk. This may make it more expensive to borrow the money needed to get a business off the ground or to grow a small startup into a more successful venture. Finding ways to boost your business credit score can help reduce or eliminate those challenges.

10 strategies for building business credit with bad personal credit

Having bad personal credit doesn’t mean building business credit is impossible. Here are a few strategies business owners can use to establish and build their business credit regardless of their personal credit score.

1: Separate personal and business finances

Creating a clear boundary between personal and business finances is a great way to start establishing positive business credit. At a minimum, business owners should open a dedicated business bank account and credit card and use those accounts for all business-related purchases.

It’s also a good idea to formalize your business structure by establishing a limited liability company (LLC) or other similar entity. This helps reduce personal liability if anything happens with the company’s finances or if you need to default on business debts.

2: Open a business bank account

Without a clear break between your personal finances and your business finances, lenders and even the IRS may not be able to tell which funds came from your business and which are part of your personal funds. Opening a dedicated business bank account is a great way to separate your business’s finances from your personal finances. Your local bank should be able to help you set up a business bank account.

You’ll typically need to bring the following with you to open the account:

- An employer identification number (EIN) for the business, available from the IRS

- A government-issued photo ID like a driver’s license or passport

- Proof of the existence of the business

- The names of your intended account owners

Every bank is different, but you’ll need to make an initial deposit to establish the account. The amount you’ll need will depend on the financial institution’s requirements.

3: Apply for a D-U-N-S number

A D-U-N-S number is a form of identification for businesses that tracks a company’s identity and makes it easier for them to develop and monitor business credit. Business owners can obtain the number from Dun & Bradstreet by visiting their website.

Here are the steps you’ll need to take:

- Choose the option from their selection that best fits your business.

- Fill out the information on the application. This will vary depending on the type of business you have.

- Choose whether to expedite the application for a small fee or wait on standard processing.

- Validate any information as needed.

You can share this number with business partners, vendors, lenders and more and use it to establish your business credit history.

4: Start with vendor credit

Some vendors will let you order products and pay them off over time. This is known as vendor credit, and it’s typically easier to qualify for than traditional loans or credit cards. When you do this and use your D-U-N-S number to associate your business with the line of credit, it can build your credit history. And as long as you make payments on time and in full, it can help build your business credit. Some vendors that work with businesses with no credit history include:

- ULINE

- Quill Corp

- Grainger

5: Apply for a secured business credit card

Secured credit cards can help you build your business credit. Unlike standard credit cards, these lines of credit are backed by a cash deposit that you make into the account. You’re able to spend up to the amount of your deposit, and paying back what you charge will positively affect your credit score.

Make sure you make payments on time and in full. If you fail to make your payments, your cash deposit will be forfeited, and you won’t boost your score. Furthermore, missing payments could cause a derogatory mark on your business credit report and may even hurt your personal credit score.

6: Consider alternative financing options

If your personal credit score is too low to let you qualify for a traditional business loan, you may be able to secure financing through one of these alternative methods:

- Microloans: These are small loans available to small business owners who may not qualify for other types of loans. These microloans can be hard to get, and many businesses may not qualify.

- Peer-to-peer lending: This method allows you to borrow money from individuals rather than lenders. It’s easier to qualify for, even for people with bad credit. These loans can have higher interest rates than other options.

- Crowdfunding: You may be able to gain capital from individuals by asking them to crowdfund your company or contribute money to your business in exchange for a small token like a sticker, t-shirt or other similar item. No credit checks are involved, and you could qualify for a larger amount than you would with traditional options.

Consider your needs and what you’re comfortable with as you explore alternative financing options.

7: Leverage business assets and revenue

You may be able to qualify for traditional loans by using business assets like equipment or inventory as collateral. If you default on the loan, the lender will be able to sell that collateral to settle what you owe.

This form of financing can help you get money if your credit score is too low to qualify for unsecured loans and as you make payments, the loan can help build your business credit score. However, if you default on the loan, you risk losing the items you used as collateral, so it’s not without risk.

8: Pay your bills on time

Arguably, the best way to build your business credit score (and your personal credit score, for that matter) is to pay your bills on time. This regular pattern of behavior shows lenders that you’re responsible. Consider setting up automatic payments or reminders for upcoming bills so you never miss a due date.

Remember, missing payments can cause both your business and personal credit scores to drop over time. Furthermore, doing so can make it hard to qualify for loans in the future.

Mobile version | File name: how-to-build-business-credit-in-10-steps | Alt text: Table showing how to build business credit in ten steps.

9. Rebuild your personal credit simultaneously

It’s worth noting that you can build your personal credit as you’re building your business credit, and doing so can strengthen your business credit in the long run. By reducing your personal debt, only applying for new loans if you truly need them and using your credit responsibly, you’ll see your score increase over time.

Once your personal credit score is strong, you may find it easier to qualify for loans with lenders who consider your personal score alongside your business credit score.

10: Monitor your business credit reports

Get in the habit of checking your business credit reports often. This will help you track your progress and ensure your score is moving in the right direction.

You may be able to check your business credit report through the bank where you opened your business bank account. Often, financial institutions let you do this for free. If your bank doesn’t offer this service, you could check your score with Dun & Bradstreet for free or use Experian to view your report for a small fee.

Monitor your report for errors, accounts you didn’t open and anything that looks off. If you see evidence of fraudulent activity or inaccurate information on your report, notify the credit bureaus immediately. You can dispute those inaccuracies by filing a 609 letter and may see your score improve once they remove the errors from your report.

Don’t let personal credit hold your business back

Though a low personal credit score can make establishing a good credit score for your business more difficult, it’s still possible. When building business credit with bad personal credit, focus on separating your business from your personal finances and always pay your bills on time and in full. Be sure to review your credit report regularly to monitor it for errors.

If you notice any errors and need help correcting them, Lexington Law Firm may be able to help. Learn more about our credit repair service.

Business credit with bad credit FAQ

Does personal credit affect business credit?

Personal credit can affect your business credit when you’re just getting started. Low scores can make it harder to qualify for financing and, ultimately, build your business’s credit score. That said, building business credit with bad credit is still possible.

How long does it typically take to build business credit?

The exact amount of time it will take to build business credit can vary based on your financial situation. However, most businesses can expect it to take about 12 months to build a solid credit history. Keep in mind that you may be able to use a business credit card to build credit and boost your score more quickly.

Can I check my business credit score like I do for personal credit?

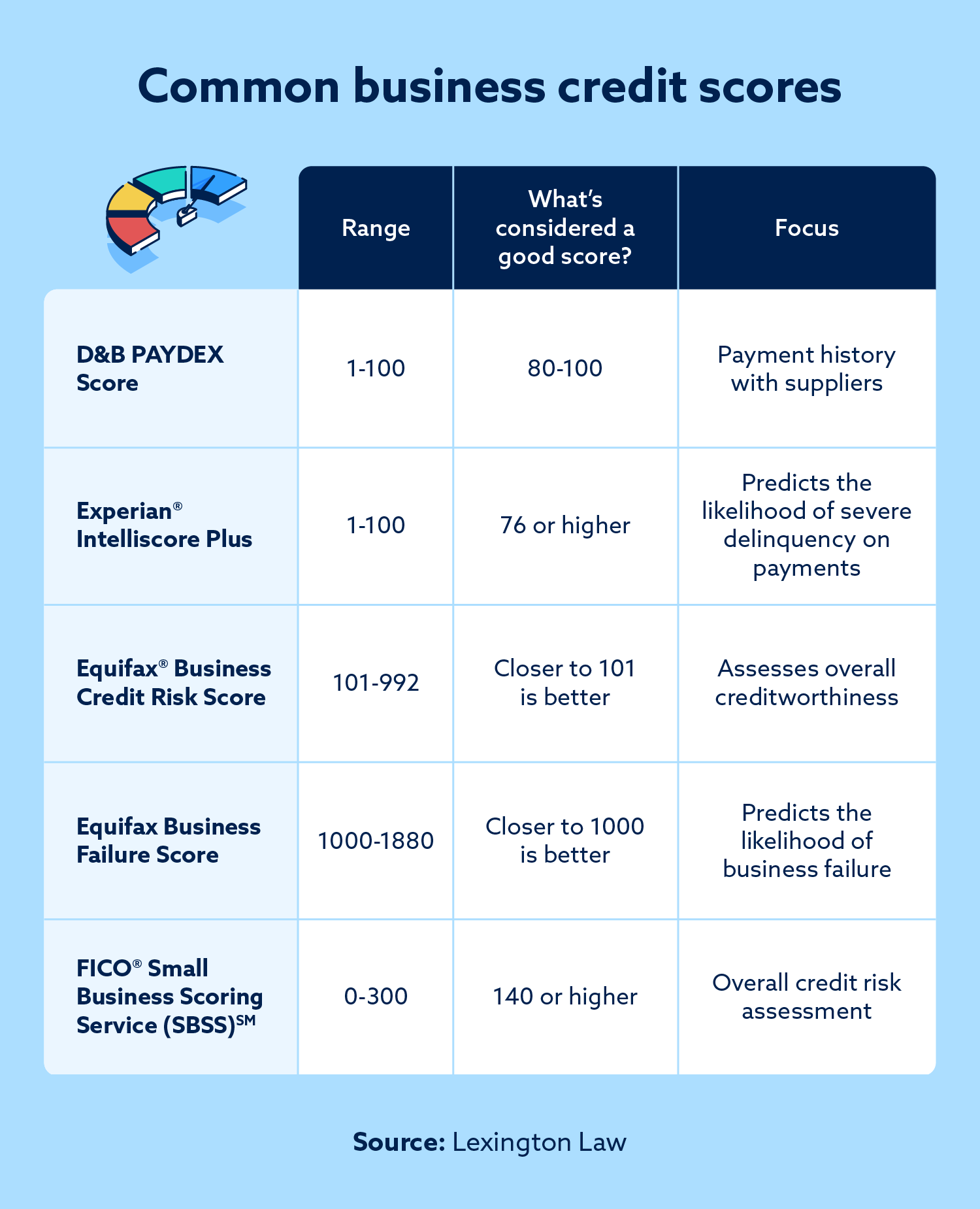

You can. Your business credit score is available from Dun & Bradstreet for free, but you can also view your report through two of the major credit bureaus, Experian and Equifax. Keep in mind that it’s still a good idea to check your personal credit score often.

Can I get a business loan with a 500 credit score?

Every lender has different requirements, and some may be willing to issue a loan with a credit score of 500. Contact each lender you’re interested in and find out their requirements before you apply. If you can’t secure a traditional loan, you may be able to get money through alternative methods like crowdfunding and peer-to-peer lending. These are among the best ways to build business credit when your personal score is lacking.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.